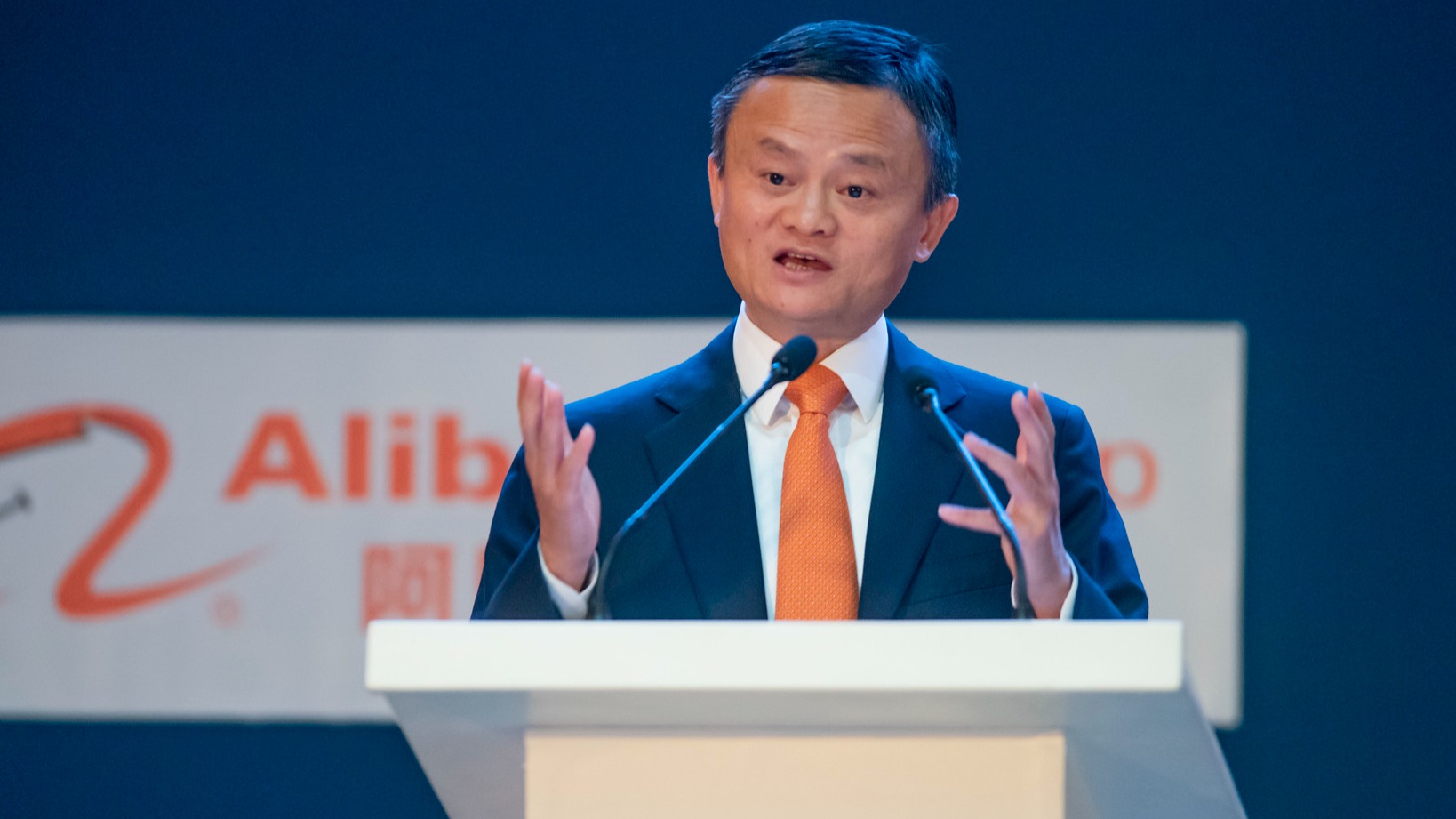

China’s fifth-richest man Jack Ma has agreed to give up control of FinTech giant Ant Group as part of a wider overhaul at the company.

The company has been facing regulatory scrutiny since its record-breaking $37 billion IPO was cancelled at the last minute in November 2020. This led to a forced restructuring of Ant Group and speculation that Ma would be pressured to step down in an effort to draw a line under the affair, with Chinese authorities still poised to impose a fine of more than $1 billion on the company.

Ant Group operates Alipay, the world’s largest mobile payments app with more than 1 billion users. The group’s business also includes consumer lending and insurance products distribution.

Ma, who rose to prominence as the founder of ecommerce behemoth Alibaba, will reduce his control of Ant Group voting rights from 50 per cent to 6.2 per cent. While Ma only owns a 10 per cent stake in the FinTech, he has been able to exert greater control via related entities such as his investment vehicle Hangzhou Yunbo.

The company said that Ma and nine other major shareholders have agreed to no longer act in concert and that they will only vote independently, though its shareholders’ economic interests will not change.

Ant Group also said that it will add a fifth independent director to its board, stating: "As a result, there will no longer be a situation where a direct or indirect shareholder will have sole or joint control over Ant Group.”

The Chinese government has carried out a crackdown on the country’s tech giants over the past two years, reducing the sector’s value by billions of dollars and cutting profits. Authorities however in recent months have softened their stance with the sector struggling to recover from the Covid-19 pandemic.

Latest News

-

JPMorgan chief ‘scouting CEOs for cross-sector AI group’

-

ABN Amro forms partnership with Mistral AI

-

Windfall tax on UK banks 'could raise £19bn' say campaigners

-

SEC creates specialist accounting enforcement unit to tackle fraud

-

Jayne Opperman to leave Lloyds following restructure

-

CFPB staff faced warning over aggressive oversight of financial companies

Creating value together: Strategic partnerships in the age of GCCs

As Global Capability Centres reshape the financial services landscape, one question stands out: how do leading banks balance in-house innovation with strategic partnerships to drive real transformation?

Data trust in the AI era: Building customer confidence through responsible banking

In the second episode of FStech’s three-part video podcast series sponsored by HCLTech, Sudip Lahiri, Executive Vice President & Head of Financial Services for Europe & UKI at HCLTech examines the critical relationship between data trust, transparency, and responsible AI implementation in financial services.

Banking's GenAI evolution: Beyond the hype, building the future

In the first episode of a three-part video podcast series sponsored by HCLTech, Sudip Lahiri, Executive Vice President & Head of Financial Services for Europe & UKI at HCLTech explores how financial institutions can navigate the transformative potential of Generative AI while building lasting foundations for innovation.

Beyond compliance: Building unshakeable operational resilience in financial services

In today's rapidly evolving financial landscape, operational resilience has become a critical focus for institutions worldwide. As regulatory requirements grow more complex and cyber threats, particularly ransomware, become increasingly sophisticated, financial services providers must adapt and strengthen their defences. The intersection of compliance, technology, and security presents both challenges and opportunities.

© 2019 Perspective Publishing Privacy & Cookies

Recent Stories