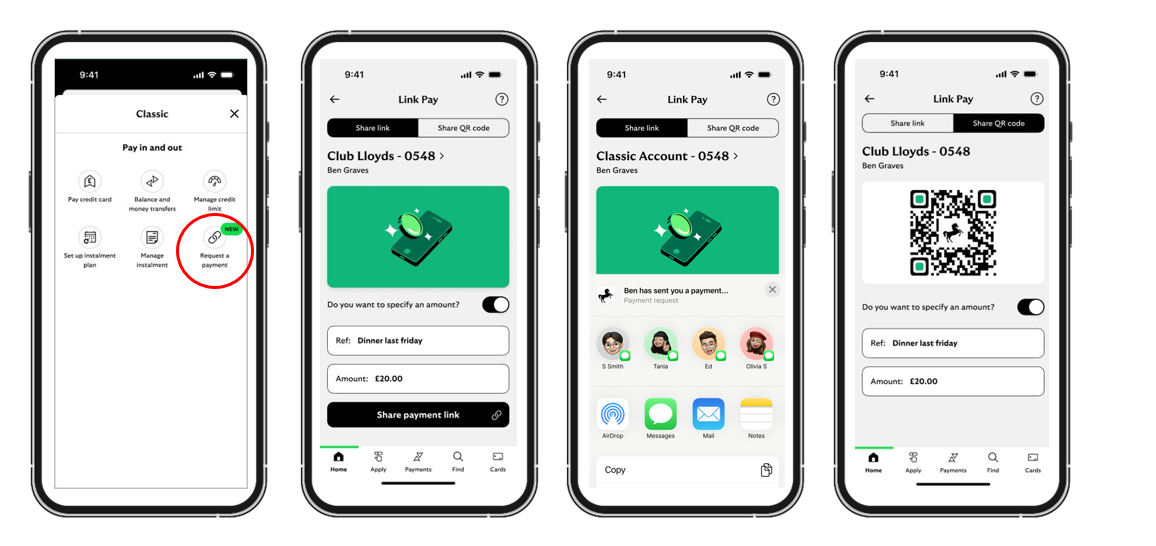

Lloyds Banking Group has introduced a new Open Banking feature that allows customers to request money from friends and family on its mobile banking app.

Link Pay enables users to request money back for shared purchases like restaurant bills or joint presents.

Lloyds customers can now send a request with a unique link or show a QR code, which means they don't need to share personal account details.

The link pre-populates all the information needed, using Open Banking to take the sender straight to their own banking app to make the payment without asking for any other details.

The request, which can be sent via WhatsApp, SMS or Facebook Messenger, is then sent straight to the person who owes money.

The new feature lets customers personalise the request with an amount and a reference, which removes the need to set up a new payee.

Customers can request up to £150 each time and receive a maximum of £500 per day.

“We want our customers to have simple, secure ways to move money at their fingertips and our new Link Pay feature in our app helps them do just that," said Gabby Collins, payments director at Lloyds. "No need to dig out a sort code and account number when someone owes you money – just add the amount and what the payment is for, and we’ll handle the rest.

"It’s never been simpler to get your sibling to repay you for Dad’s birthday gift.”

Latest News

-

Jamie Dimon likens Claude Mythos risks to giving civilians ‘ballistic missiles’

-

NatWest joins quantum programme to explore fraud detection use cases

-

Revolut set to begin offering crypto in UAE after regulatory approval

-

Stripe ‘makes $53bn bid’ for PayPal in partnership with private equity group

-

BNPL services come under full FCA enforcement

-

BBVA uses generative AI to analyse customer interactions

Creating value together: Strategic partnerships in the age of GCCs

As Global Capability Centres reshape the financial services landscape, one question stands out: how do leading banks balance in-house innovation with strategic partnerships to drive real transformation?

Data trust in the AI era: Building customer confidence through responsible banking

In the second episode of FStech’s three-part video podcast series sponsored by HCLTech, Sudip Lahiri, Executive Vice President & Head of Financial Services for Europe & UKI at HCLTech examines the critical relationship between data trust, transparency, and responsible AI implementation in financial services.

Banking's GenAI evolution: Beyond the hype, building the future

In the first episode of a three-part video podcast series sponsored by HCLTech, Sudip Lahiri, Executive Vice President & Head of Financial Services for Europe & UKI at HCLTech explores how financial institutions can navigate the transformative potential of Generative AI while building lasting foundations for innovation.

Beyond compliance: Building unshakeable operational resilience in financial services

In today's rapidly evolving financial landscape, operational resilience has become a critical focus for institutions worldwide. As regulatory requirements grow more complex and cyber threats, particularly ransomware, become increasingly sophisticated, financial services providers must adapt and strengthen their defences. The intersection of compliance, technology, and security presents both challenges and opportunities.

© 2019 Perspective Publishing Privacy & Cookies

Recent Stories